Two formulas cover almost every GST calculation in Australia. A third covers the property margin scheme. Once those three are mental shorthand, the rest is bookkeeping.

This is the reference page for each: the maths, the algebra behind why the numbers work, the spreadsheet versions and the edge cases that come up if you sell property, second-hand goods or run a mixed BAS line.

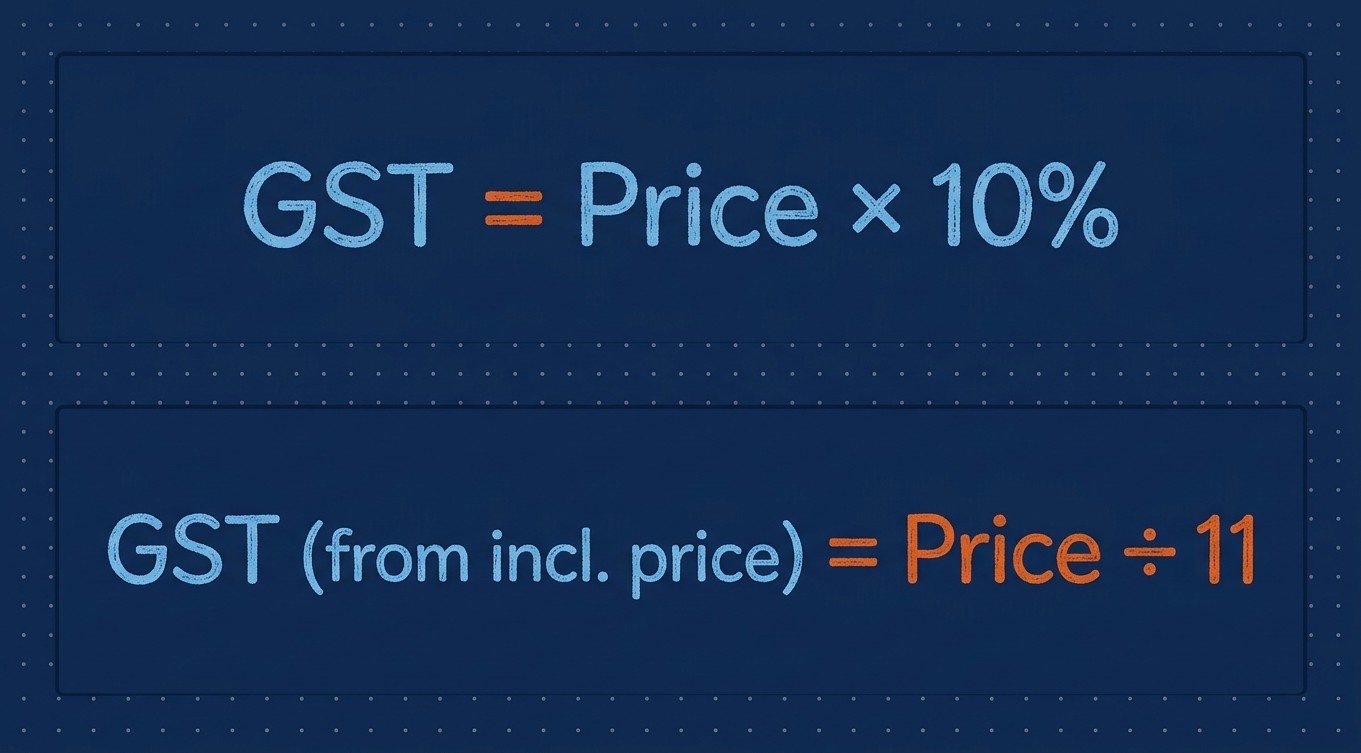

The two everyday formulas

Add GST to a net price:

Net × 1.10 = Gross

Remove GST from a gross price:

Gross ÷ 11 = GST

Gross ÷ 1.10 = Net (excluding GST)

That’s it for 95% of invoices, receipts and quotes. ASIC’s MoneySmart calculator confirms the same two: ‘multiply the amount exclusive of GST by 1.1’ to add it, and ‘divide a GST inclusive cost by 11 to work out the GST component’.

If you only ever go one direction, the Add GST calculator and Reverse GST calculator skip the dropdown and head straight to the input. The home-page GST calculator handles both in one tool.

Why divide by 11, not 10

This is where new BAS lodgers slip.

GST is 10% on the net price, not on the gross. If the net is $100, the GST is $10 and the gross is $110. Of that $110, the GST component is $10, which is 10/110 – simplified, that’s 1/11.

Working through the algebra in plain terms:

- Let net = N, gross = G, rate = r = 0.10

- G = N × (1 + r) = N × 1.10

- Therefore N = G ÷ 1.10

- And GST = G − N = G − (G ÷ 1.10) = G × (1 − 1/1.10) = G × (0.10 / 1.10) = G ÷ 11

The clean answer is that GST is one-eleventh of the inclusive total. Dividing a gross figure by 10 over-states the GST line by roughly 10% – a small error that compounds through a quarter and shows up as a bad BAS reconciliation at the end of it.

Equivalent forms of the same formula

The two formulas can be written half a dozen ways depending on which figure you start with. They all give the same answer.

- Add GST: Net × 1.10 = Gross. Equivalent forms: Net + (Net × 0.10) = Gross, or Net × 11 ÷ 10 = Gross.

- GST from net: Net × 0.10 = GST. Or Net ÷ 10 = GST.

- GST from gross: Gross ÷ 11 = GST. Or Gross × (1/11) = GST. Or Gross × 0.0909 (rounded) = GST.

- Net from gross: Gross ÷ 1.10 = Net. Or Gross × 10/11 = Net. Or Gross − (Gross ÷ 11) = Net.

Pick whichever feels cleaner in the head. Multiplying by 11/10 is faster on a phone calculator with no decimal key; dividing by 11 is faster on paper.

Spreadsheet formulas (Excel and Google Sheets)

If you do this work weekly, copy these into a template and you won’t type them again. Cell A2 holds the input figure.

- Add GST to a net price (A2): =A2*1.1

- GST component from a gross price (A2): =A2/11

- Net from a gross price (A2): =A2/1.1

- GST and net from a flagged figure – with B2 holding TRUE if A2 is gross, FALSE if net: =IF(B2,A2/11,A2*0.1) for the GST line, =IF(B2,A2/1.1,A2) for the net.

A round-to-cents wrapper is usually worth adding: =ROUND(A2/11,2) keeps the BAS column free of fractional cents.

The margin scheme formula (property only)

The margin scheme is the special case that catches property developers, subdividers and anyone selling residential land that wasn’t bought as a fully taxable supply. It applies to property only.

The ATO publishes the formula plainly: under the margin scheme, the GST payable is one-eleventh of the margin. The margin itself can be calculated two ways:

- Consideration method. Margin = sale price − original purchase price.

- Valuation method. Margin = sale price − approved valuation. Used when the property was acquired before 1 July 2000 or under specific circumstances the ATO sets out in its margin-scheme rulings.

A worked example from the ATO’s own published material. A property sells for $515,000 after being bought for $150,000. The margin is $365,000. The GST payable is $365,000 ÷ 11 = $33,181 – not 10% of $515,000, which would be $51,500. The difference is the developer’s saving and the reason the scheme exists.

When the margin scheme is used, the purchaser can’t claim a GST credit on the sale, even if they are GST-registered. Property accountants treat margin-scheme deals as a separate line of work for that reason.

BAS formulas: 1A and 1B

The Business Activity Statement nets a quarter into a single payable figure using two cells.

- 1A: GST on sales. Total GST collected from customers. Sum of the GST line on every tax invoice you issued.

- 1B: GST on purchases. Total GST paid to suppliers. Sum of the GST line on every tax invoice you received that relates to your business.

Net BAS GST = 1A − 1B

If 1A is bigger than 1B, you owe the ATO. If 1B is bigger – common in the first quarter of a new business that has bought stock or equipment – the ATO refunds the difference.

The ATO publishes a free interactive GST calculation worksheet that handles each line of the BAS automatically. We use it as a sanity check against bookkeeping-software output before lodging.

Edge cases the everyday formulas don’t cover

A handful of supply types need different handling, and the ÷ 11 shortcut won’t always apply:

- Second-hand goods bought from non-GST-registered sellers. A dealer who buys a car privately and resells it through their yard can claim a notional GST credit on the purchase. The credit is still one-eleventh of the buy price, but the rules around eligibility are tighter than the formula suggests.

- Mixed-supply receipts. A grocery docket that mixes GST-free fresh food with GST-inclusive household goods can’t be divided by 11 wholesale. Use the receipt’s printed GST line, not the formula.

- GST-free supplies. Most basic food, most education, most health services, child care and exports are GST-free. The formula stays at zero – there’s no GST to add or remove.

- Input-taxed supplies. Financial services and residential rent. No GST charged, no GST credit claimed. The formula does not apply.

- Imports and customs. GST on imported goods is calculated on the customs value plus duty plus international transport and insurance, not on the supplier’s invoice price. The Australian Border Force’s published rules govern this one.

If your starting figure touches any of those categories, use the line-by-line GST shown on the document, not a blanket formula across the total.

Worked examples

A simple set, in the order they show up in real bookkeeping.

- Tradie quote (add GST). Net $720 × 1.10 = $792 gross. GST line: $72.

- Bunnings receipt (remove GST). Gross $187 ÷ 11 = $17 GST. Net: $170.

- Annual contract (add GST). Net $4,500 × 1.10 = $4,950 gross. GST line: $450.

- Reverse a ‘GST inclusive’ price tag at JB Hi-Fi. Gross $99 ÷ 11 = $9 GST. Net: $90.

- Property developer (margin scheme). Sale $620,000, purchase $260,000, margin $360,000. GST: $360,000 ÷ 11 = $32,727.

One last thing

If you want a single formula that survives most situations and is hard to misremember, write ‘GST = Gross ÷ 11’ on the inside cover of your invoice book. Every other version unpacks from there. For everything else – the margin scheme, the BAS, the imports rule – the ATO’s How GST works page is the official starting point, and the Reverse GST calculator is a quicker way to spot-check your spreadsheet against the formula.

- Australian Taxation Office – How GST works

- Australian Taxation Office – Methods to calculate the margin (margin scheme)

- Australian Taxation Office – Calculating the GST payable (margin scheme)

- Australian Taxation Office – Interactive GST calculation worksheet for BAS

- Australian Taxation Office – GST-free sales

- ASIC MoneySmart – GST calculator